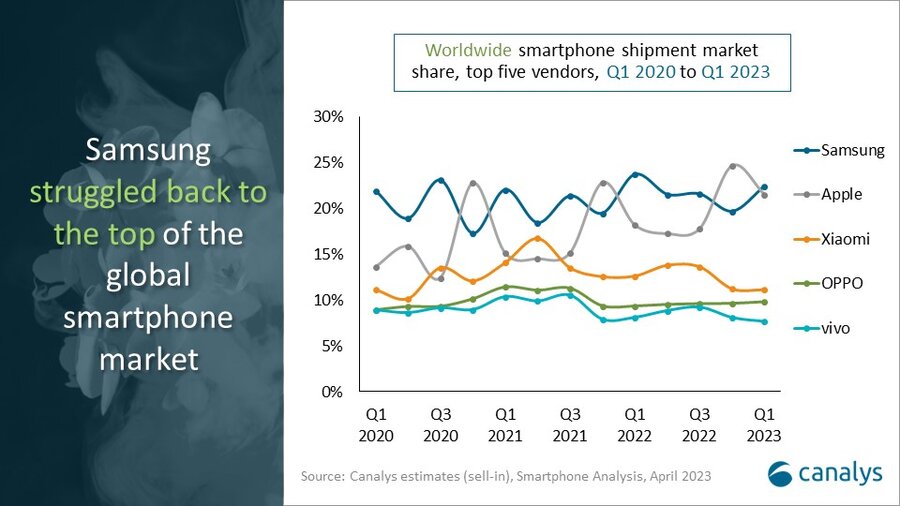

According to the newest report by Canalys, Samsung managed to reach the top position for Worldwide smartphone shipment market share in Q1 2023.

The South Korean tech giant finished the first quarter of 2023 with a 22% market share for smartphones, closely followed by Apple at 21%.

In Q1 2023, the worldwide smartphone market sustained its fifth consecutive quarterly decline, declining by 12% year-on-year. Despite some modest improvements in major macroeconomic factors, the market has yet to see a full recovery. Nevertheless, Samsung was the only leading company to achieve quarter-on-quarter growth.

The same report also mentions that Xiaomi maintained its position as the third-largest smartphone vendor in the world, with a market share that remained steady in the last quarter. Meanwhile, BBK Electronics’ brands Oppo and Vivo secured the fourth and fifth positions, respectively, with market shares of 11% and 10%, indicating strong growth.

Checkout my other article: Global PC and Mobile Gaming Revenue Fell to $92.3 Billion in 2022

These companies have a significant presence in various Asian and European markets, particularly in the lower-priced smartphone segment, which has been a key driver of their success. It’s worth noting that while they have not yet made significant inroads in the US market, they have established themselves as major players in other regions.

Canalys believes that the next few quarters will see a recovery in smartphone sales, propelled by the surge in 5G adoption and the emergence of inventive designs such as foldables.

Canalys Analyst Sanyam Chaurasia said in its official release, “The smartphone market’s decline in the first quarter of 2023 was within expectations throughout the industry. The local macroeconomic conditions continued to hinder vendors’ investments and operations in several markets. Despite price cuts and heavy promotions from vendors, consumer demand remained sluggish, particularly in the low-end segment due to high inflation affecting consumer confidence and spending. Additionally, the continuous sluggish end-user demand has triggered a major wave of destocking across the entire supply chain, with channels reducing inventory levels to secure operations. To maintain a low level of sell-in volume, vendors continued to use cautious production techniques, which had a long-term negative impact on the component supply chain’s operational performance.”

Feat Image: Torsten Dettlaff via Pexels