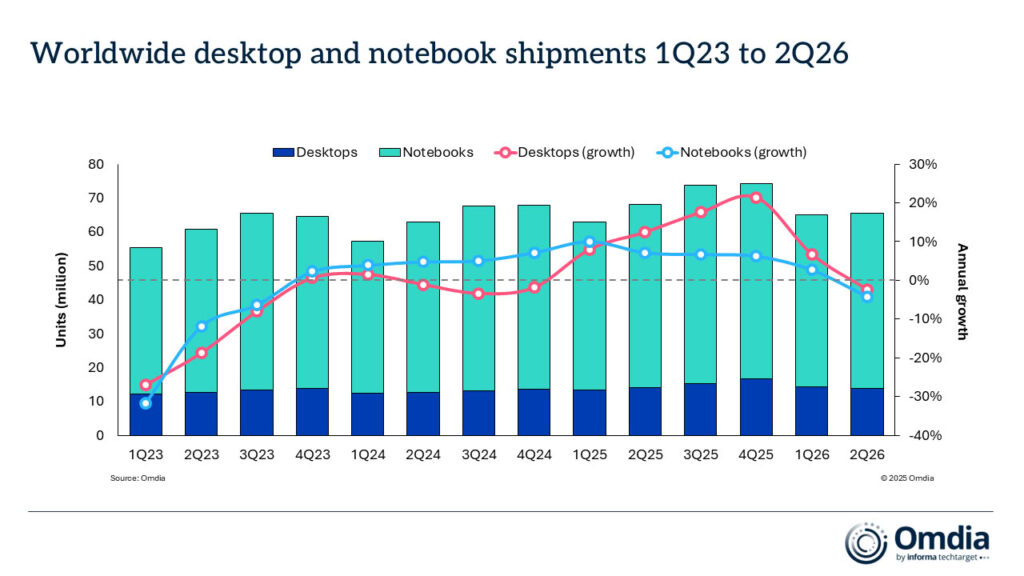

The global PC market lost momentum in the second quarter of 2026, with shipments of desktops, notebooks, and workstations falling 3.6% year over year to 65.7 million units, according to Omdia.

At first glance, that decline looks relatively modest. Dig deeper, however, and the market is wrestling with a much less comfortable problem: rising component costs are pushing PC prices sharply higher just as businesses and consumers are becoming more cautious about upgrades.

The result is a market caught between purchases that were pulled forward earlier in the year and demand that may now be postponed until prices settle down. Unfortunately for buyers, “settling down” does not appear to mean “getting cheaper” anytime soon.

Notebook Shipments Take the Bigger Hit

Notebook shipments, including mobile workstations, reached 51.7 million units during the quarter. That represented a 4.2% decline compared with the same period last year.

Desktop shipments, including desktop workstations, held up slightly better. Vendors shipped 13.9 million units, down 1.3% year over year.

The figures suggest that the broader decline was driven primarily by portable PCs, which account for the majority of industry volume. Notebooks are also particularly sensitive to increases in memory and storage costs because vendors have less flexibility to swap components or absorb additional expenses within tightly integrated designs.

Component Inflation Is Reaching the Checkout Page

Sharp increases in memory and storage prices during the first quarter began affecting finished PC prices in the second quarter.

According to Omdia, the prospect of further price increases encouraged some consumers and IT departments to purchase machines earlier than planned. That helped keep sales volumes relatively stable for a period, but it may have borrowed demand from future quarters.

In other words, the market did not necessarily create more buyers. It simply convinced some of them to arrive early before the price tags became even more unpleasant.

Vendors have been raising prices since late 2025, with comparable PC product lines now costing roughly 20% to 40% more than they did a year ago. Apple’s recent MacBook price increases have attracted plenty of attention, but the company is far from alone. Other major manufacturers began adjusting prices as early as the fourth quarter of 2025 and have continued doing so throughout 2026.

Businesses Are Delaying Refresh Cycles

The commercial PC market could face an especially difficult second half.

More than half of the business-to-business channel partners surveyed by Omdia in June said their customers were postponing planned hardware refreshes until market conditions become more predictable. Another 6% believed some customers could cancel purchases altogether.

That hesitation comes at an awkward moment for corporate IT departments.

The market is approaching the first anniversary of Microsoft’s October 2025 Windows 10 end-of-support deadline, yet many organizations still have large fleets of older PCs that need to be replaced or upgraded.

Normally, that backlog would provide a useful source of demand. Instead, businesses now have to balance the security and support risks of aging hardware against significantly higher replacement costs. That is not much of a choice, but it is certainly an excellent way to make an IT budget develop trust issues.

PC Prices Are Unlikely to Fall Soon

Omdia expects the pace of memory and storage cost increases to slow during the second half of 2026. However, slower inflation does not mean that component prices will reverse.

Neither memory nor storage prices are currently expected to fall before the end of the year. Meanwhile, other components are becoming more expensive, including:

- Multilayer ceramic capacitors, commonly known as MLCCs

- Printed circuit boards

- Additional supporting electronic components

PC vendors will therefore continue dealing with elevated manufacturing costs even after the most dramatic price increases begin to ease.

Those costs are likely to remain reflected in retail and commercial pricing throughout the second half of the year. Manufacturers can absorb some pressure, but margins are not magical cushions with infinite stuffing. Eventually, much of the added expense reaches the customer.

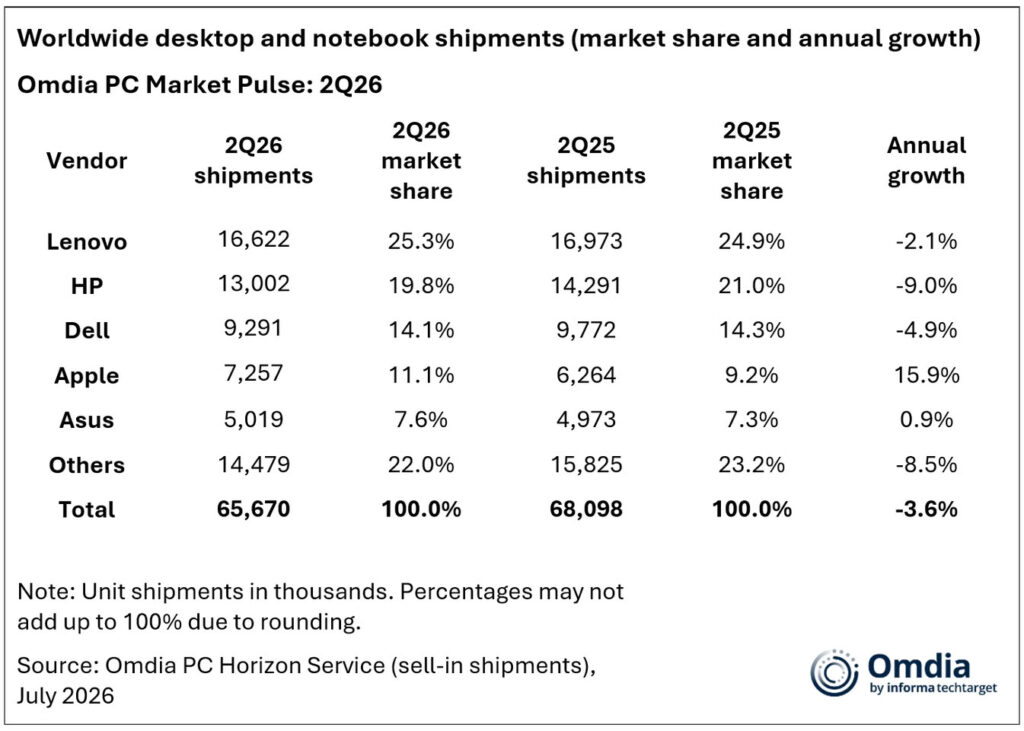

Lenovo Holds the Lead While Apple Gains Ground

Lenovo remained the world’s largest PC vendor in the second quarter, shipping 16.6 million units. Its shipments declined by a modest 2%, but the company maintained a market share of approximately 25%.

HP stayed in second place with 13 million units shipped. Its performance was considerably weaker, with volume falling 9% from the previous year.

Dell ranked third after shipping 9.3 million units and capturing around 14% of the market. Its results showed relative resilience despite component shortages and broader pricing pressure.

Apple delivered the strongest growth among the five largest vendors. The company shipped 7.3 million Macs, supported by the launch of the MacBook Neo and continued underlying demand. Apple also gained two percentage points of market share compared with the second quarter of 2025.

ASUS completed the top five with shipments of 5 million units, remaining broadly unchanged from the previous year.

Apple’s Growth Shows Buyers Will Still Pay for the Right Product

Apple’s performance is particularly noteworthy because it occurred alongside higher MacBook prices.

That does not necessarily mean customers are unconcerned about pricing. Instead, it suggests that strong product launches and a differentiated ecosystem can provide some protection when the broader market weakens.

Apple is generally less dependent on low-margin entry-level volume than many Windows PC vendors. It also controls more of its hardware and software stack, allowing it to position new systems around performance, efficiency, and integration rather than specifications alone.

However, even Apple is not immune to prolonged component inflation. Premium buyers may tolerate one increase, but repeated price adjustments eventually test how premium that loyalty really is.

A Difficult Second Half Is Taking Shape

The PC industry is entering the second half of 2026 with several competing forces.

Commercial fleets still need upgrades. Windows 10’s end of support remains a powerful reason for businesses to replace aging machines. New product launches could also stimulate demand, particularly if vendors introduce meaningful improvements in performance, battery life, or artificial intelligence features.

At the same time, higher prices are making customers delay purchases, while the demand brought forward earlier in the year leaves fewer immediate buyers in the pipeline.

This creates the risk of a temporary demand gap: customers know they need new PCs, but many are unwilling to purchase them at current prices.

The Industry Takeaway

The second-quarter shipment decline is not simply another sign of weak PC demand. It reflects a market being reshaped by component inflation, aggressive price increases, and increasingly cautious upgrade decisions.

Demand has not disappeared. Much of it has merely been delayed.

That distinction matters because postponed purchases can eventually return, especially in the commercial market where older systems cannot remain in service indefinitely. But unless component costs ease faster than expected, the PC industry may spend the rest of 2026 discovering just how long buyers are willing to keep their current machines alive.

Given the price of replacements, that five-year-old laptop may suddenly look surprisingly youthful.