The PC market was supposed to be settling into something resembling normal. Not exciting, not disastrous, just the usual cycle of upgrades, discounts, and people pretending their five-year-old laptop is “still fine.” Instead, 2026 is shaping up to be another rough year, with global PC shipments projected to fall sharply as component costs surge.

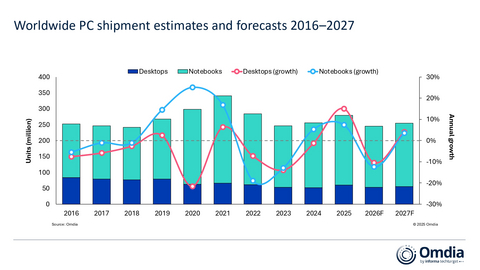

According to Omdia’s latest outlook, worldwide shipments of desktops, notebooks, and workstations are expected to drop 12% in 2026, landing at 245 million units. And this is not one of those vague “macroeconomic uncertainty” forecasts that gets wheeled out whenever analysts want to sound mysterious. The problem is much more specific: memory and storage are getting expensive fast, and the entire PC supply chain is about to feel it.

The Real Culprit: Memory and Storage Sticker Shock

At the center of the slowdown is a steep jump in the cost of memory and storage. Omdia expects prices for these components to rise by at least 60% in the first quarter of 2026 alone. That is not a gentle nudge upward. That is the kind of increase that makes hardware vendors stare silently at spreadsheets for a very long time.

Since the first quarter of 2025, the cost of mainstream memory and storage configurations has already climbed by roughly $90 to $165. For PC makers, that is a nasty hit in a market where margins are already thin and consumers are trained to expect deals every other weekend.

The result is predictable, if not exactly fun:

- Fewer promotions

- Higher retail prices

- More aggressive cost-cutting on configurations

- Tougher decisions about which products deserve the best components

In other words, the era of “more RAM, bigger SSD, same price” is taking a sabbatical.

Desktops and Laptops Both Take a Hit

This is not just a laptop problem or a desktop problem. It is a broad PC market problem.

Omdia expects desktop shipments to fall 10% to 53.2 million units in 2026. Laptops, which make up the bulk of the market, are forecast to decline 12% to 192.2 million units.

That consistency matters. It suggests this is less about one product category losing appeal and more about a supply-side squeeze hitting the whole industry at once. When the expensive bits get even more expensive, everybody gets dragged into the mess.

The Downside Case Looks Uncomfortably Real

Here is where things get even less cheerful. Omdia is not treating this 12% decline as a worst-case scenario. The firm says the forecast still carries significant downside risk, especially if shortages widen and component pricing climbs even further.

Under a harsher scenario, PC shipments could fall 15% or more in 2026.

That is a meaningful difference. A 12% decline is painful. A 15% drop starts to feel like the market getting shoved down a staircase.

There is also a geopolitical wildcard in play. The recent conflict in the Middle East has added fresh uncertainty around international logistics and regional demand. It is still unclear how lasting that disruption will be, but it is one more variable in a market that was already having enough problems without new shipping headaches.

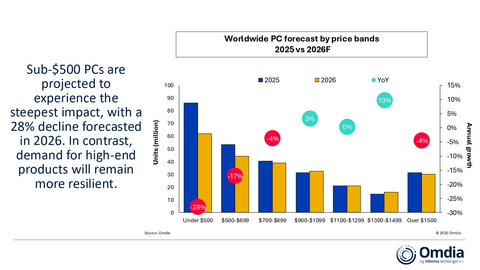

Cheap PCs Are Getting Squeezed the Hardest

Not all parts of the market will suffer equally. The lowest-priced PCs are expected to take the biggest hit, and honestly, that tracks.

Systems priced below $500 are forecast to plunge 28% to about 62.1 million units in 2026. That is brutal, but it makes sense for a few reasons.

First, budget devices have very little room to absorb rising component costs. A premium laptop can hide a cost increase behind branding, industrial design, and the magic phrase “AI-ready.” A bargain machine does not have that luxury. If its bill of materials jumps, the pain shows up immediately.

Second, lower-end products often depend on older, lower-capacity components. Those are exactly the kinds of parts that may face lower allocation priority or get phased out by suppliers altogether. So vendors are not just dealing with cost pressure. In some cases, they may struggle to get the parts they want at all.

That leaves PC makers with an obvious strategy: protect higher-end products first.

Check out my other article: Why Smartphone Batteries Suddenly Matter More Than Speed

Premium PCs May Actually Hold Up

While the low end gets hammered, systems priced at $900 and above are expected to perform far better and may even post modest growth.

That does not necessarily mean consumers are suddenly eager to splurge. It means the buyers who truly need a PC, whether they are professionals, businesses, or higher-income consumers, are more willing to accept higher prices. Vendors are also more motivated to prioritize premium models because the margins are better and the business case is easier to defend.

There is a subtle but important point here. An upward shift in average selling price does not automatically mean the machines themselves are getting better.

A more expensive PC in 2026 may simply be a PC that costs more to build, not one with meaningfully improved specs. Paying more for the same capacity is not exactly the kind of innovation anyone was hoping for.

Platform Winners and Losers: Windows, Chrome, Mac, and HarmonyOS

The supply crunch is also expected to hit PC platforms differently.

Windows PCs: Big Market, Big Exposure

Windows systems, which account for 83% of shipments, are forecast to decline 12% in 2026. That is roughly in line with the broader market, but because Windows dominates overall volume, it will absorb most of the industry pain in absolute terms.

There is no mystery here. The biggest platform tends to catch the biggest wave when the market goes sideways.

Chrome Devices: The Biggest Casualty

Chrome devices are expected to suffer the steepest decline, down 28%.

That is especially significant because Chromebooks are heavily tied to education and lower-cost deployments, two areas that are highly exposed to the exact pressures Omdia is highlighting: low margins, tight component allocation, and dependence on older or lower-capacity parts. When supply gets constrained, these products are often first in line to be deprioritized.

It is a rough setup for a category that already relies on cost discipline to stay compelling.

Macs: Not Immune, but Better Insulated

Mac shipments are forecast to decline a more modest 5%.

Apple’s vertically integrated supply chain and premium positioning give it a cushion that many rivals do not have. When the industry hits turbulence, controlling more of the stack tends to be useful. Funny how that works.

Apple is not escaping the downturn entirely, but it is clearly better positioned to absorb the blow than vendors fighting over commodity parts in the Windows ecosystem.

HarmonyOS PCs: Small Base, Big Growth

Then there is HarmonyOS, which is expected to grow tenfold year over year from a small base as Huawei expands its PC ecosystem in China.

That does not make it a global market heavyweight overnight, but it is still notable. In a year when most of the PC industry is looking for the least painful way to shrink, any platform showing breakout growth deserves attention, even if the starting point is modest.

What This Means for the Industry

The big takeaway is that 2026 is not shaping up to be a demand-led correction. This is a supply-driven downturn, and that changes the logic for everyone involved.

PC vendors will likely spend the year doing three things at once:

1. Protecting Profitability

Expect companies to focus more on premium models and business devices, where they have a better chance of preserving margins.

2. Trimming Value at the Low End

Budget PCs may not disappear, but buyers should prepare for weaker specs, fewer promotions, and less attractive configurations.

3. Rethinking Product Mix

Vendors may increasingly steer customers into higher price bands, not because the market suddenly became more upscale, but because that is where the economics still work.

That is the slightly absurd part of this whole story. The market may shift upward in price even as actual consumer value gets murkier.

The Bottom Line

The PC industry is heading into 2026 with a serious component problem, and the fallout looks widespread. Omdia’s forecast of a 12% shipment decline already paints a bleak picture, but the real story is how uneven the damage could be.

Budget PCs look especially vulnerable. Chromebooks may get clobbered. Premium systems should hold up better. Apple seems relatively sheltered. Huawei’s HarmonyOS push could be one of the few genuine growth stories in the category.

Mostly, though, this is a reminder that the PC business still lives and dies by the supply chain. You can have all the AI branding, flashy industrial design, and keynote optimism in the world, but when memory and storage prices explode, gravity tends to win.

And in 2026, gravity looks very much in charge.